Investing in the age of AI

How COinvest Builds its Portfolio for a World in Rapid Transition

As we build the COinvest portfolio: the classic investor question used to be what will this asset be worth? That question hasn’t gone away, but it’s no longer sufficient. The more pressing question, increasingly, is will the activity that this asset depends on still exist in its current form five years from now?

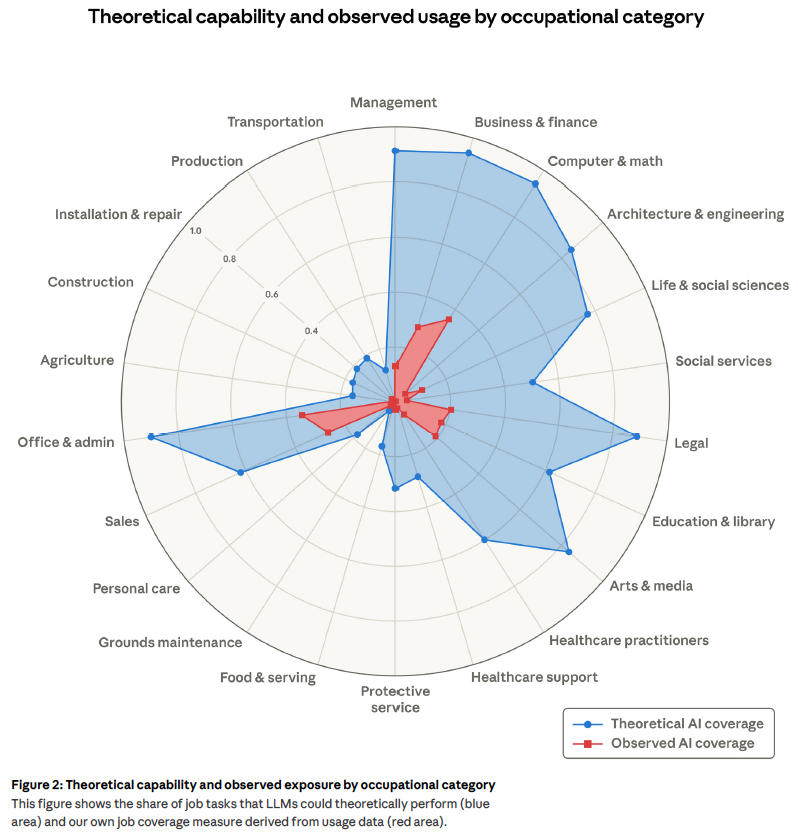

The challenge we face is that the pace of AI development is being measured in weeks, not decades. Software companies that looked impregnable two years ago are watching AI tools replicate their core functionality. Professional services firms are seeing decades of expertise being commoditized in real time. Entire categories of white-collar work — paralegal research, financial analysis, content creation — are being restructured as we speak. Anthropic recently released a report projecting which jobs are most exposed to AI disruption and how much AI has penetrated these roles. What we found most striking was the rather binary impact between those most at risk and least at risk. The sectors least at risk had scores below 20% of job tasks at risk, while those most exposed were often above 90%.

source: Labor market impacts of AI: A new measure and early evidence

For investors deploying capital over five- to ten-year horizons, this demands a genuinely different way of thinking about where to put that capital. And we’d argue that most of the frameworks investors are currently using weren’t designed for this pace of change.

The Asymmetry That Matters

Not all industries face the same AI exposure — and understanding that asymmetry is one of the main factors in how we’re thinking about portfolio construction at COinvest.

The distinction we keep coming back to is this: businesses that create value primarily in the digital world — aggregating data, producing reports, generating content, providing analysis — face genuine existential risk from AI agents that can do the same work faster, cheaper, and without taking breaks. But businesses that create value primarily in the physical world are a meaningfully different story.

Consider the contrast. A software platform that produces data-driven reports faces real disruption risk. A company that installs heat pumps in homes does not. The heat pump still needs to be manufactured, delivered, and physically installed by someone who shows up with tools and training. New windows still need to be fitted. Farmland still needs to be cultivated by farmers who understand their land. For this kind of work, AI can make people more efficient — better scheduling, smarter procurement, predictive maintenance — but it can’t replace the work itself.

This is not an anti-technology thesis. We are not bearish on AI, far from it. But we do believe that some of the most durable investments over the coming decade will share a common trait: their core value creation happens in the physical world, where there’s always a human touch at the center of the business model. AI may accelerate the work, but it can’t substitute it.

What We’re Looking For

Given the almost weekly pace of new AI model introductions, we’re seeking investments where the underlying activity is resistant to displacement and, ideally, where AI serves as an accelerant rather than a threat. That’s led us toward physical infrastructure, essential services, tangible assets, and the kinds of skilled trades and real-world operations that will remain indispensable regardless of how capable these models become.

Below we walk through several strategies in our current portfolio that illustrate how this plays out in practice.

Arborview III: The Built Environment

Arborview III invests in companies delivering the physical products and services that homes and buildings require. Two portfolio companies exemplify what we find compelling here: Alpen Technologies, which manufactures windows, and Elephant Energy, which installs electrification solutions for residential properties.

These are not businesses a chatbot can disrupt. Someone needs to manufacture the glass, assemble the frame, and install the window. Someone needs to assess a home’s existing mechanical systems, spec the right heat pump, and wire it into the electrical panel. The work is physical, skilled, and local. It also sits squarely in the path of powerful secular tailwinds: aging housing stock, building electrification mandates, and growing consumer demand for energy efficiency. Skeptics might argue that automation and robotics are how AI will eventually threaten these industries, and I think that’s worth taking seriously. But we haven’t seen it, and we don’t see credible medium-term threats from robotics in these sectors.

Where AI adds value here is at the edges — better scheduling algorithms, predictive maintenance, smarter procurement — without touching the core activity. These companies are likely to see AI-driven efficiency gains while facing essentially zero risk that AI eliminates the need for their products or services.

Kah Capital III: Non-Performing Mortgages and the Human Element

Kah Capital III pursues a strategy centered on acquiring non-performing residential mortgages and working with homeowners to modify their loans, bring them current, and keep them in their homes. The result is a portfolio that generates compelling risk-adjusted returns while simultaneously preserving homeownership for families that might otherwise face a short sale or foreclosure.

The reason this strategy holds up well in an AI-driven environment is straightforward: the underlying asset is a home and a mortgage, and the value creation depends on navigating complex, highly regulated, and deeply human interactions. Loan modifications require working through federal and state regulatory frameworks, negotiating with servicers, and engaging with individual borrowers in circumstances that are often financially and emotionally fraught. While AI may streamline certain back-office functions — document processing, borrower communication workflows — the judgment, regulatory expertise, and relational skill at the core of this work are earned over years of experience, not encoded in a model.

I’ll also be direct about one risk here: if AI displaces large numbers of jobs and unemployment rises significantly, that could make Kah’s model more challenging. But this team has navigated periods of high unemployment over the past two decades, and we believe their experience and underwriting insights give them the tools to manage that risk. More broadly, the asset class itself — residential real estate collateral — is inherently physical and inflation-hedged in ways that digital assets simply can’t be.

Apis and Heritage: Preserving the Trades Through Employee Ownership

Apis and Heritage provides mezzanine financing for employee stock ownership plan (ESOP) buyouts of small and mid-sized businesses. The types of companies transacting through this structure are telling: construction firms, landscape architecture companies, and similar trade- and service-oriented businesses where the work product is inherently physical.

This strategy is doubly insulated from AI disruption. First, the businesses themselves operate in sectors where the core work — pouring concrete, grading land, designing and installing outdoor spaces — can’t be replicated by software. If anything, these industries are facing severe labor shortages, which makes the businesses more valuable, not less, as the economy evolves.

Second, the financial structure itself — mezzanine debt secured by the ESOP transaction — is a well-understood credit instrument that doesn’t depend on aggressive growth and technology-oriented assumptions for its return profile. That’s the kind of clean, grounded thesis we find compelling right now.

In Our Pipeline: Organic Agricultural Land Conversion

We’re also evaluating a strategy that acquires conventional agricultural land and transitions it to USDA-certified organic production. The thesis combines real asset ownership with an operational value-creation lever: organic farmland generates meaningfully higher per-acre income through organic price premiums, and the conversion process itself — typically a three-year transition — creates a definable, time-bound path to value enhancement.

Farmland might be the most AI-resistant asset class in existence. The land is finite and non-replicable. The organic transition process is biological and regulatory — soil chemistry must change over years, not quarters, and USDA certification requires sustained demonstrated practice. No algorithm can accelerate the biology of soil remediation or shortcut the bureaucracy of organic certification.

And yet — and this is part of what makes the thesis compelling — this is a strategy where AI can genuinely add value at the operational level. Precision agriculture, satellite-based crop monitoring, predictive models for pest management and soil health, AI-optimized supply chain logistics: all of these can improve yields and reduce costs for organic producers. The farmer-operators who partner with this fund can be made more productive by the very technology that threatens to displace knowledge workers elsewhere in the economy. Even robotics, which is still early days on farms, would likely be an accelerant to returns rather than a threat.

Beyond improving farmer incomes with greater revenue, the investment also carries a meaningful environmental dimension: reducing synthetic pesticide and fertilizer use, improving soil health, and increasing carbon sequestration.

A Note on Technology-Enabled Businesses

We want to be careful not to suggest that all software or technology-enabled businesses are equally at risk, because we don’t think that’s right.

If we look at some of the venture funds in Gary Community Ventures’ portfolio, several are heavily invested in software and technology-enabled business models. But we’re finding that some of them still have an embedded human component that makes AI disintermediation less likely. Proprietary data, genuine network effects, regulatory requirements, meaningful human relationships at the core of the business — these are the features that separate the more durable technology investments from the more fragile ones. Indeed even within COinvest’s portfolio, Resilience VC is an example where regulatory requirements often play a mitigating role in the current impact of AI.

So the questions we’re now asking of any technology investment are: what’s the defensible moat here? What does this company have that an AI can’t replicate? If the answers are compelling, we’re still interested. If they’re not, we’re considerably more cautious than we would have been three years ago.

The Bigger Picture

The common thread across these strategies isn’t a rejection of technology. It’s a recognition that the most important question for long-term investors right now isn’t how do we invest in AI? It’s how do we invest in a world being reshaped by AI?

Two main takeaways from this line of thinking are:

1. The physical economy offers some of the most durable investment opportunities of the next decade. Homes that need to be built and upgraded. Land that must be cultivated. Mortgages backed by real property. Businesses where people show up and do work that no model can replicate. These assets will endure through technological transitions — and in many cases will be enhanced by the very capabilities that render other investments obsolete.

2. For technology and software-enabled businesses, the bar is higher now than it was. The question isn’t just whether a company has a good product or strong growth today. It’s whether it has something proprietary — data, relationships, regulatory position, network effects — that meaningfully protects it from being replicated or replaced by increasingly capable AI systems.

At COinvest, we’re building a portfolio that will overindex not just for Colorado but for the physical world. And as the digital world undergoes its most profound transformation in a generation, we think that’s a great place to be.